January began bumpy as investors assessed prospects for 2024 following a strong 2023. Following this, markets closed the month up as confidence returned. The S&P 500 hit a new record high, driven mainly through shares in semiconductor companies such as AMD and Nvidia.

All three major US indices are up 100% from their pandemic lows (i.e., investors who entered the US markets at their bottom in 2020 would now have doubled their money in less than four years).

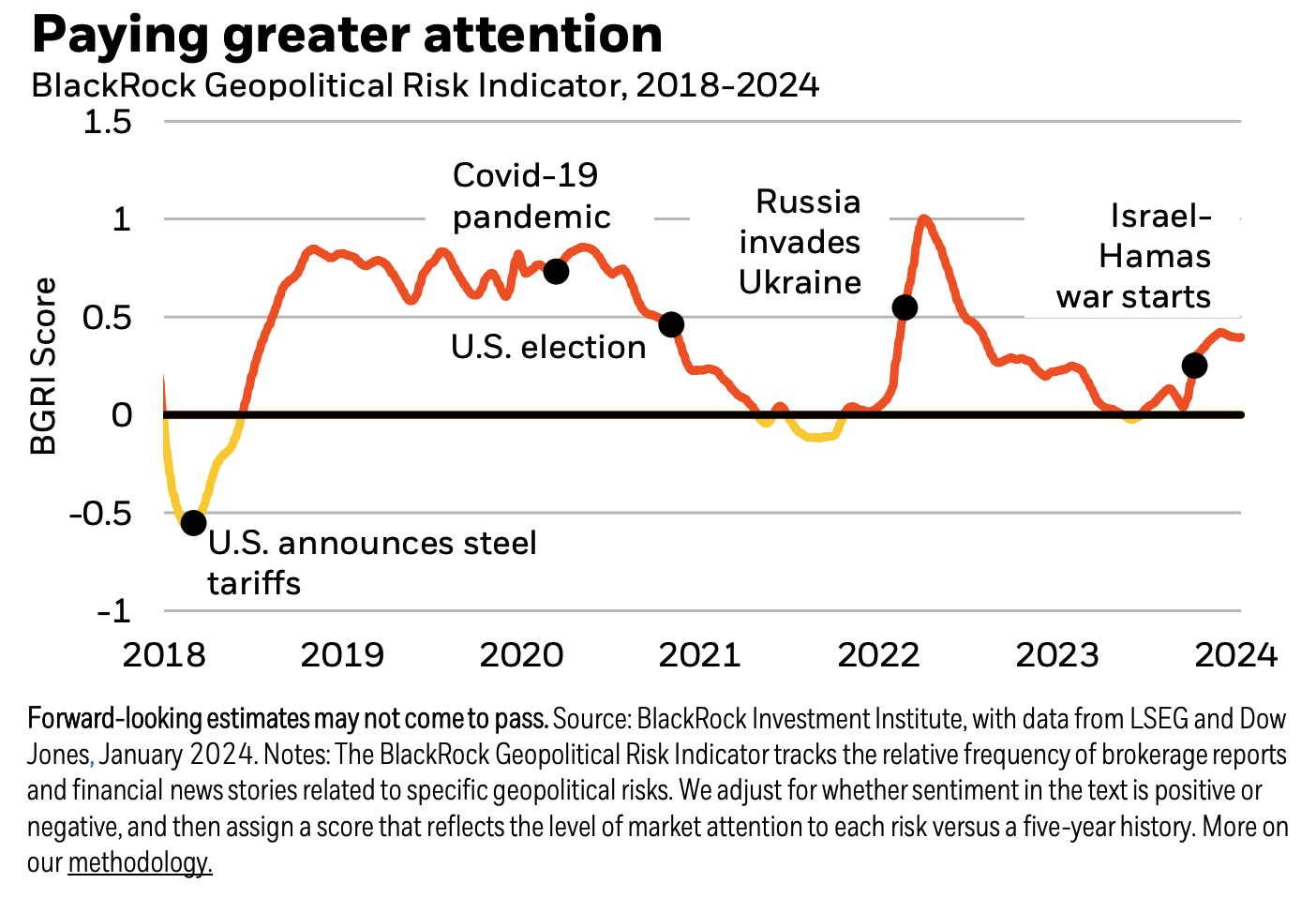

The World Bank has forecast that the global economy will grow just 2.4% in 2024 due to a trade slowdown caused by higher interest rates and global conflicts. This would be the slowest rate of growth since the pandemic.

Headline CPI in the US for December came in at 3.4%, up from 3.1% in November. However, core CPI, which excludes food and energy prices, fell from 4% to 3.9%, suggesting other price pressures are continuing to ease. The Fed’s preferred inflation measure, the core personal consumption expenditures price index, fell from 3.2% to 2.9% year-on-year. Wholesale inflation also fell, with the producer price index declining 0.1% in December.

The US economy grew at a much stronger rate than anticipated in Q4, with annualised growth of 3.3% against forecasts of 2%. This left the US with growth for the whole of 2023 at 2.5%, up from 1.9% in 2022. Recession expectations have been withdrawn by most economists, and now the expectation is for continued growth in 2024, albeit at a slower pace than last year.

Home sales fell to their lowest level in 30 years due to rising interest rates and increased prices caused by tight supply. The median sales price is 40% higher than in 2019.

Looking ahead, despite some rebalancing of demand and supply in the labour market, the US still added a further 216,000 jobs in December and 353,000 in January, defying expectations of a slowdown and much higher than expected. The US also continues to have historically low unemployment and strong wage growth. It won’t necessarily be a smooth ride for the US from here, but the hopes of achieving a ‘soft landing’ are growing for many market participants.

The Fed signalled last year that its policy rate had peaked, and investors have begun to price in rate cuts for this year. The consensus shows that the market expects the first cut to happen in May. The Fed chose to leave rates unchanged at the end of January. It signalled that further improvements in the data would be needed before cuts are introduced.

The British economy grew 0.3% in November, which was stronger than expected. However, the three months to the end of November were negative for GDP growth, leaving the UK at risk of recession should the economy fail to grow in December (this would mean two consecutive quarters of contraction in Q3 and Q4 of 2023).

Inflation in the UK also rose against the trend in December, at 4% compared to November’s 3.9% and higher than the expectations of 3.8%.

This puts the Bank of England in a difficult position, as inflation remains too high for them to consider rate cuts. However, a recession may necessitate them to boost growth. The risks of central bank policy error are higher here than in the US.

Many European workers anticipate wage increases this year, which could hamper the ECB’s efforts to get inflation down to its 2% target. The ECB expects salary increases this year, on average, of 4.6%, much higher than the 3% it believes to be the maximum to keep inflation at 2%. Higher wages lead to higher costs for firms and more household income to spend, both of which contribute to inflation. This is why the ECB sees wage growth as the biggest risk to its fight against inflation.

Having ended its hiking cycle in September, the ECB decided to keep interest rates at 4%, believing it too soon to begin introducing cuts. There was, however, an openness to a change of message in March at the Bank’s next meeting. This wouldn’t see rate cuts happen then but could pave the way for the first one to occur in June, should the data on inflation support doing so.

The Chinese economy grew by 5.2% last year, just above the government’s target of 5%. The prime minister said no major stimulus packages would be needed to achieve an economic rebound. As we have mentioned before, having spent most of 2022 in lockdowns against Covid-19 and when GDP growth was just 3%, achieving 5.2% growth in 2023 is nothing for investors to get excited about.

The property market continues to be a source of concern, with prices declining for the seventh consecutive month. Most wealth in China is tied up in property, so falling prices heavily impact consumer balance sheets. The embattled property giant Evergrande, with debts of over $300 billion, was ordered to liquidate by a Hong Kong court over failing to provide a restructuring plan. The order applies to its Hong Kong-based holding company, but enforcement may prove difficult as most of its assets are held in mainland China.

The People’s Bank of China left its one-year policy loan rate unchanged despite expectations of a first cut since August.

China’s stock markets continue to struggle, with the CSI 300 hitting a five-year low. Hong Kong’s Hang Seng Index has also been trading near its lowest since 2009; Hong Kong was recently overtaken by India as the fourth-largest equity market in the world (by combined value of shares).

China became the world’s largest vehicle exporter in 2023, sending 5.3 million vehicles overseas, compared to the 4.3 million sold by Japan. Petrol cars were the largest portion of its exports. However, the electric car market within China is growing rapidly, with a 22% increase in electric car sales compared to 2022. BYD is now the world’s biggest seller of electric cars, overtaking Tesla to take the top spot (526,000 units sold in Q4 2023 versus 485,000).

In big news for crypto investors, the Securities and Exchange Commission (SEC), the US financial regulator, approved the first, much-anticipated Bitcoin ETFs. This is a milestone moment for the cryptocurrency asset class, as it now gives investors exposure to Bitcoin through a regulated instrument. Bitcoin has increased in value by 70% in recent months (ironically, it is still valued against the centralised US dollar) to its highest level since late 2021, with much speculation around this decision likely already being priced in.

The SEC stressed that its decision was not an endorsement or approval of Bitcoin, with the chair describing the cryptocurrency as “primarily a speculative, volatile asset that’s also used for illicit activity.”

Our view is that crypto remains a speculative and very high-risk asset class, and we do not recommend cryptocurrency investments as part of our proposition.

Recent attacks by the Houthis in Yemen on shipping containers passing through the Red Sea on their way to the Suez Canal are driving shipping costs back up. This is auspiciously in retaliation against the US and UK for supporting Israel’s war on Hamas. However, ships with seemingly dubious ties, or no ties, to either country are also being targeted. The Houthis are backed and armed by Iran, and the US and UK have responded by sending warships to the region and targeting Houthi missile sites with airstrikes.

Ships from Asia now have to choose between the dangers of passing through the Red Sea (they will also face increased insurance costs) or taking the long way around the African continent to reach Europe. The latter option has also been argued to be emboldening a resurgence in attacks by Somali pirates.

Shipping costs were a significant driver of inflation immediately after the pandemic, so rising costs again now when inflation has been reducing is likely not positive for policy rate decisions by central banks. Further to this, the risk of a proxy conflict spilling out into a wider regional conflict (Iranian-backed militias have also been striking US bases, recently killing three soldiers in Jordan) is causing markets to pay more attention to geopolitics.

Conflict and geopolitics in the Middle East will be a big talking point in this year’s US presidential election and a concern for many governments worldwide.